THE EDGE. 17TH AUGUST: The Johor Bahru property market has shown signs of improvement, thanks to the reopening of borders in April last year and the spillover effect of impending investments on the property market, says KGV International Property Consultants (Johor) Sdn Bhd executive director Samuel Tan in presenting The Edge | KGV International Property Consultants Johor Bahru Housing Property Monitor 1Q2023.

He cites examples of high-profile impending foreign direct investments such as Tesla’s potential investment in Tesla Experience and Service Centres as well as the supercharger network; the potential RM170 billion in investments from China, with RM80 billion coming from Rongsheng Petrochemical Co Ltd, following a recent visit to China led by Prime Minister Datuk Seri Anwar Ibrahim; and the potential RM24 billion investment from South Korea involving Samsung Engineering, SKC, Lotte Fine Chemicals, Hyundai, COWAY and a consortium of South Korean companies.

Tan believes these investments in the pipeline are a good start to revive the economy. “Malaysia’s pro-business stance appears to be bearing fruit. Hopefully, we are able to convert such announcements into realised investment and more investment streams will continue to flow into Malaysia. Johor, being a proactive state, has also been a forerunner in attracting investment in oil and gas, palm oil, data centres and other manufacturing projects in recent years.

“We have all the necessary ingredients to be at the forefront of attracting foreign investment. The property market will benefit as a result and, hopefully, it will be supported by solid investments that create job opportunities and broaden the spin-off benefits, not just a simple game of property construction and short-term speculation,” he says.

Macroeconomic factors

The country’s gross domestic product grew 5.6% in 1Q2023, which Tan says is not exceptional but still a respectable performance. It is higher than the 4.8% growth achieved in 1Q2022.

Tan attributes this growth to the country’s business sentiment, which appears to have improved in view of the investments streaming in. Other macroeconomic factors that have contributed to growth in first-quarter GDP are the rise in the overnight policy rate (OPR) and the possibility of more connectivity infrastructure being built to link Johor with Singapore.

In May this year, Bank Negara Malaysia raised the OPR to 3%, from 2.75%. Tan says the country’s OPR is now back to pre-pandemic levels. “The current interest rate is still not excessive. Nevertheless, the increment of 125 basis points from 1.75% to the current 3% still weighs heavily on buyers’ repayment ability. Developers will have to juggle the issues of lower buyer affordability and a higher cost base due to an increase in construction and labor costs.”

In efforts to ease connectivity and provide alternative routes from Johor Bahru to Singapore, Tan suggests a few initiatives that can be adopted by the government such as introducing ferry services between Puteri Harbour and Tuas; or building a third bridge to enhance the connectivity between Johor Bahru and Singapore..

“Apart from the Johor Bahru-Singapore Rapid Transit System (RTS Link) that is well underway, there is talk about a possible revival of the Kuala Lumpur-Singapore

High-Speed Rail (HSR), to be spearheaded by the private sector,” he adds.

Both countries will benefit from having better connectivity in the long run, says Tan. “In view of high property prices and escalating rental [rates] in land-scarce Singapore in recent years, better connectivity between the two countries will be a win-win proposition for the two. It is possible for Johor Bahru to be an alternate hub, complementary to the republic down south, as a venue for accommodation, workplace and manufacturing facility.”

Supply and price trends

According to Tan, residential property transaction volume and value in 1Q2023 showed an upward trend of 43% and 57% year on year respectively. Residential transaction volume in 1Q2023 fell 4.9% quarter on quarter whereas transaction value rose 5.1%.

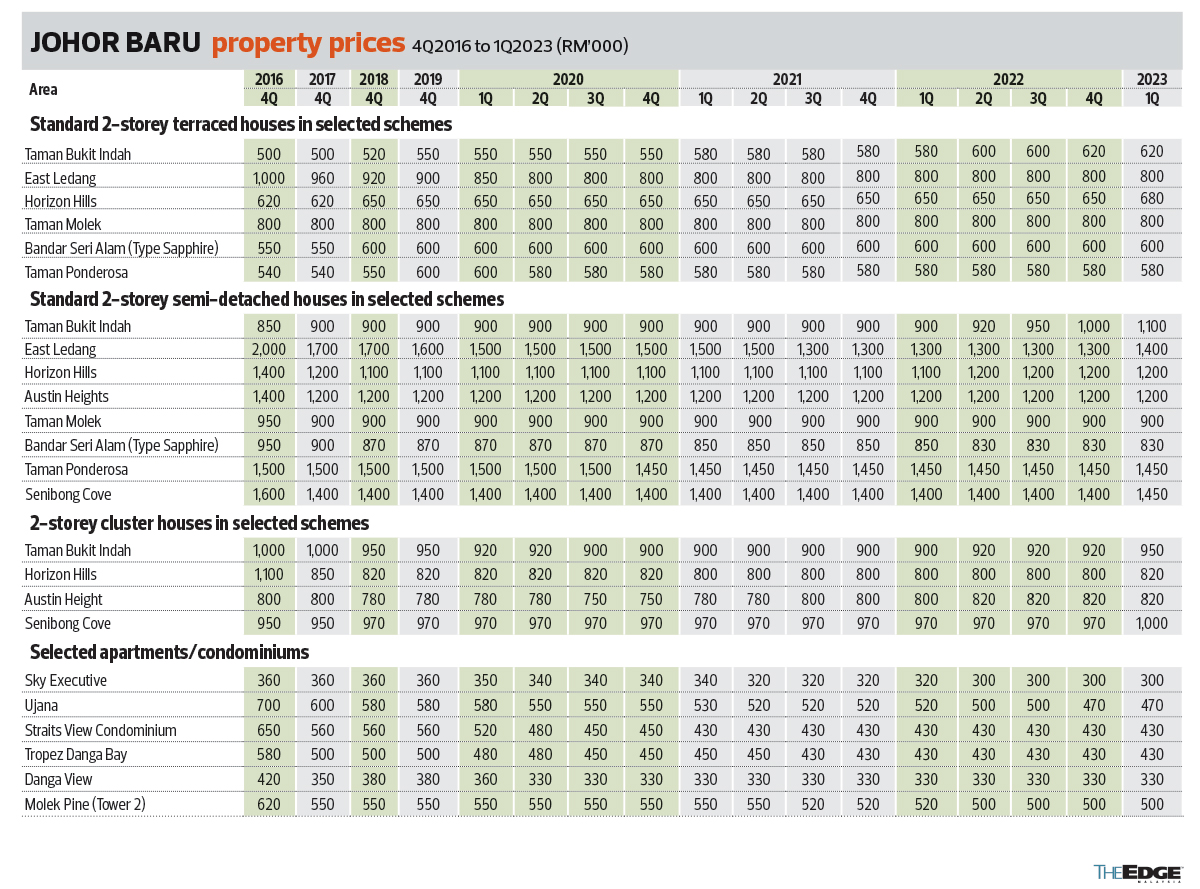

There were seven new launches in 4Q2022 — four in Mukim Pulai, two in Mukim Tebrau and one in Mukim Plentong — involving landed residential developments ranging from 2-storey terraced to 2-storey semi-detached homes. Tan says the demand for landed houses in Johor Bahru remains strong.

“This can be seen from the healthy [take-up] rate of 30% to 100% despite being launched only a few months ago. Most 2-storey terraced houses are now priced from RM700,000 to RM900,000 each. It appears that terraced houses priced in the previous ‘sweet spot’ of RM500,000 to RM600,000 are increasingly difficult to find,” Tan says.

“It is also interesting to note that developers are growing more confident and starting to launch larger landed property types such as 2-storey clusters homes and semi-detached homes. The sale performance of the larger units is also relatively healthy with some even fully sold. This is a reflection of the return of the feel-good sentiment after the extremely tough period in the past three years.”

Property overhang, on the other hand, has been a constant challenge for the Johor Bahru market, especially for high-rise residential properties. “Overhang” here refers to completed properties that have remained unsold for more than nine months.

Tan has collected data on all high-rise residential property types in Johor Bahru including condominiums, apartments, serviced apartments and SoHos. The overhang number in 1Q2023 fell 8.6% y-o-y to 17,625, from 19,285, but rose 4.9% q-o-q from 16,799 in 4Q2022.

“Based on the data, it is perhaps still too early to conclude that the property market is on a decisive upturn in Johor Bahru. But the worst is likely to be over after the unprecedented Covid-19 pandemic. The property market has recovered from the trough, with encouraging transaction volume and value, relatively manageable incoming supply and overhang statistics.

“Hopefully, the developers and authorities will be more cautious before embarking on a high-rise residential development to avoid the supply and demand mismatch as a result of ‘wrong pricing’, ‘wrong product’ and ‘wrong timing’,” Tan stresses.

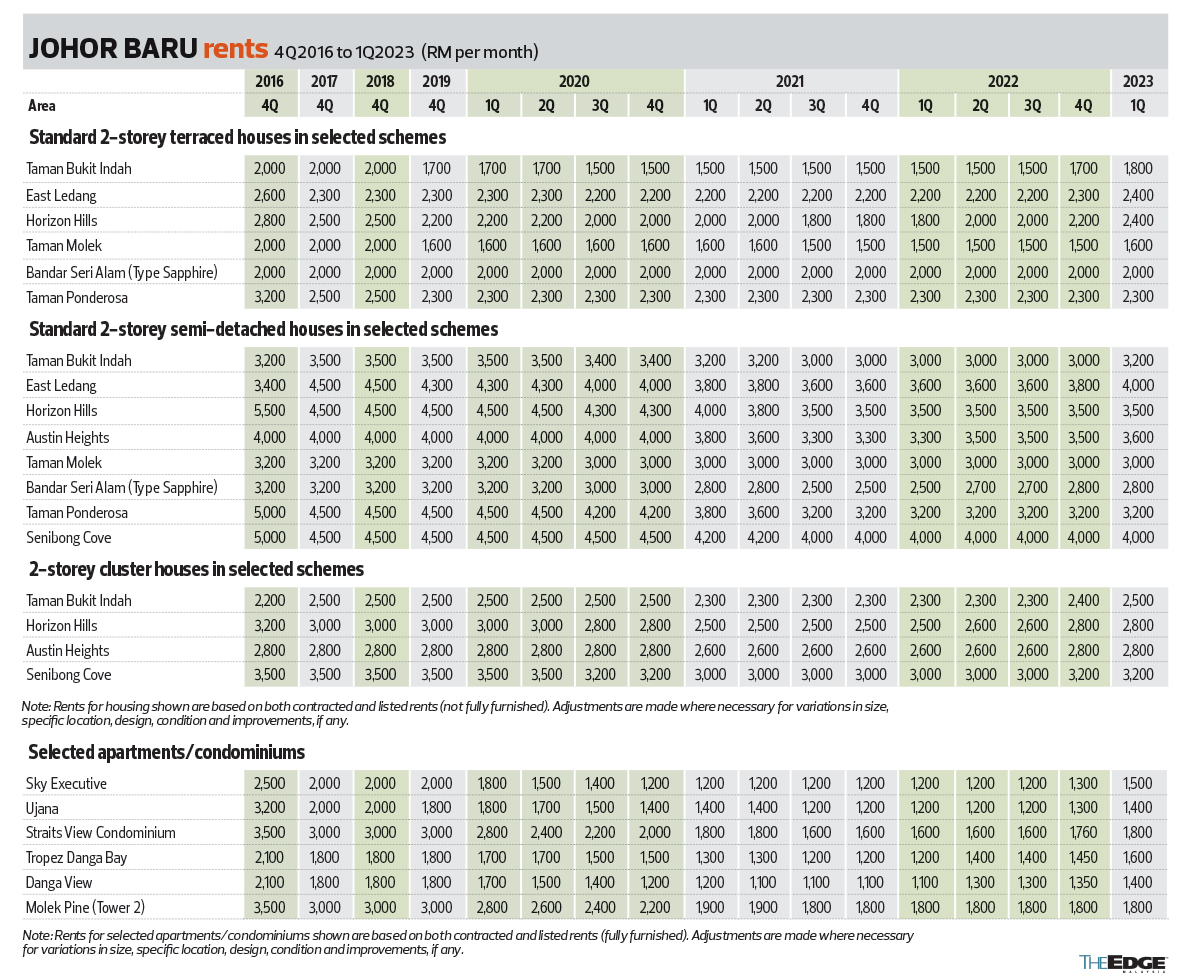

On the flip side, he says Johor Bahru’s rental market has been healthy and very active this quarter. “For landed houses, we noticed that a few popular housing estates that are easily accessible, especially to the Second Linkway, such as Bukit Indah and Horizon Hills, registered a higher-than-average growth rate of more than 5% to close to 10%.”

The monthly rent of a 1,400 sq ft, 2-storey unit in Horizon Hills rose to RM2,400 in 1Q2023, from RM2,200 in 4Q2022. Similarly, a 3,400 sq ft, 2-storey semi-detached unit also saw an increase in monthly rent to RM3,200 in 1Q2023,from RM3,000 in 4Q2022.

Tan says: “Rental rates of high-rise apartments increased across the board from 1.5% to 10.3%. We noticed that rents for high-rise residences have been increasing since the reopening of borders.”

According to the monitor, a 750 sq ft serviced apartment unit at The Sky Executive Suites at Bukit Indah recorded an increase in monthly rental to RM1,500 in 1Q2023, from RM1,300 in 4Q2022.

“The vibrant rental market is largely caused by the return of Malaysians working in Singapore. The ‘fast and furious’ rental escalation in Singapore has driven many Malaysian tenants to seek rental accommodation in Johor Bahru, especially in locations that are close to both causeways, for ease of daily commuting,” he says.

In terms of price trends, Tan says landed houses in Taman Bukit Indah and East Ledang registered increases of 2.5% to 10%, depending on the property type. He adds that 2-storey semi-detached homes in these two developments showed the highest percentage increase in absolute price of 7.7% to 10%. Meanwhile, the prices of high-rise apartments remained unchanged from 4Q2022.

Based on his observations, both resale and new property transactions also saw improved take-up because of the pent-up demand built up in the past two to three years. “The past three years probably offered some breathing space for the market to consolidate, especially for the high-rise property market,” he points out.

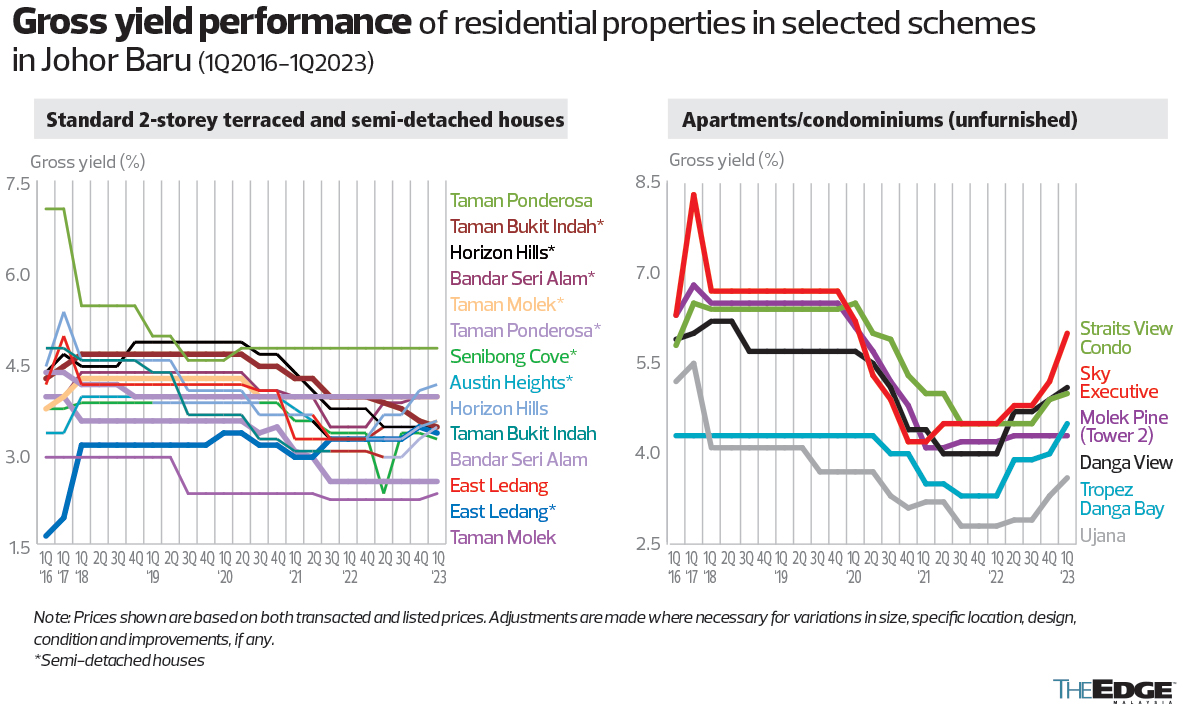

Tan says yields have grown significantly, especially for high-rises. “Yields of smaller landed houses such as 2-storey terraced homes increased in 1Q2023, owing to higher rental. For larger landed houses, the yield dropped for developments such as double-storey semi-detached units in Taman Bukit Indah, East Ledang and Senibong Hill and 2-storey clusters homes in Horizon Hill and Senibong Cove.

“This is because the price is increasing faster than rental growth in these property types. Yield returns for high-rise apartments increased across the board because of higher rental growth,” he says, adding that one of the most notable yield increases was seen at a 750 sq ft serviced apartment unit in Sky Executive that had a yield of 5.2% in 4Q2022 and 6% in 1Q2023.

Launches in 1Q2023

All property launches during the period under review were of 2-storey landed houses. Launched in January this year, Calliandra in Taman Setia Tropika, Tebrau, comprises 118 two-storey cluster homes. These fully sold units have built-ups starting from 2,602 sq ft and selling prices ranging from RM904,230 to RM1.397 million.

Also launched in January was Phase 1 of the KSL @ Pulai Bestari in Pulai, consisting of 183 two-storey terraced houses with built-ups from 2,050 sq ft and selling prices ranging from RM820,000 to RM1.33 million, with a take-up rate of 35%.

February launches include 2-storey terraced homes named Adonis (Phase 7H-1) in Plentong. This development, which is 50% sold, offers 70 units that have built-ups ranging from 1,817 to 2,733 sq ft that are priced from RM710,900 to RM1.198 million.

Another project, dubbed Phase 2C of Sapphire in the larger Crest @ Austin township in Tebrau, features 76 units of two-storey cluster homes and semi-detached homes with built-ups of 2,551 to 3,589 sq ft and selling prices of RM1.295 million to RM2.257 million. Most of these homes have been taken up.

Soft-launched in February, Phase 2A of Senadi Hills in Pulai comprises 75 two-storey terraced houses with built-ups of 2,197 to 2,330 sq ft and prices starting from RM843,000. Tan says all the non-bumiputera lots have been sold out.

Offering 84 two-storey semi-detached units, homes in Phase 3 of Danga Sutera in Pulai are priced from RM1.592 million to RM2.208 million and have built-ups of 3,014 to 3,297 sq ft. This project has been 30% taken up.

Launched in March this year, PJ 22 in Pulai comprises 2-storey cluster homes with a take-up rate of about 30%. This low-density development has only 22 units, with a built-up area of 2,023 sq ft each and selling prices starting from RM880,000.