THE EDGE. 12TH OCTOBER: By June this year, Penang’s overall property market had well and truly recovered from the impact of Covid-19, particularly since the transition to the endemic phase that started in April last year.

In the first quarter of this year, both transaction volumes and values in the state saw an improvement from one and two years ago, says CBRE | WTW director Peh Seng Yee.

“According to data released by the National Property Information Centre (Napic), a total of 5,742 properties were transacted in Penang state in 1Q2023, which reflects increases of about 10% and 19% compared to the previous corresponding periods of 1Q2022 (with 5,228 properties) and 1Q2021 (with 4,839 properties) respectively,” he notes.

“The transacted properties in 1Q2023 in the state worth about RM6.119 billion depict significant growth of more than double the value transacted in the corresponding periods in 1Q2022 (RM2.817 billion) and 1Q2021 (RM2.659 billion).”

A similar trend was observed when comparing the transactions in 2022 with those in 2021. According to Nawawi Tie Leung Property Consultants Sdn Bhd executive director Saleha Yusoff and Henry Butcher Real Estate (Penang) Sdn Bhd director Teoh Poh Huat, 23,481 properties worth RM13.38 billion were transacted in 2022, registering a 34% increase in volume and 28% in value from the previous year (2021: 17,526 properties worth RM10.45 billion transacted).

All subsectors saw an uptrend in 2021 and 2022, says Saleha. In terms of volume, the agriculture subsector saw the largest increase at 56.2%, followed by commercial (55.5%), residential (31.1%), development land (30.6%) and industrial (12.5%).

In terms of value, all subsectors recorded an upward trend as well, with agriculture seeing the largest increase at 124.9%, followed by residential (33.4%), development land (17.6%), commercial (15.4%) and industrial (0.7%). “We expect the same positive movement for 2023 as buyers and investors have regained confidence,” she says.

Meanwhile, Henry Butcher’s Teoh observes that Penang’s tourism and retail sectors have been boosted by the reopening of borders and the transition to the endemic phase, giving rise to a recovery in all subsectors, with the industrial, tourism-related and service industries taking the lead. “The performance of the property market in Penang shows a recovery driven by growth in market activity,” he says.

However, cautious optimism continues to linger in the market amid major challenges such as labour shortage, currency instability, higher material cost, interest rate hikes, supply chain disruption, affordability concerns with property prices increasing faster than income levels, rising cost of living, and scarce sizeable development land, say the property consultants.

Best performers

The residential property segment continued to be the most vibrant and active subsector in Penang, accounting for 76.2% of transaction volume and 59.5% of transaction value in 2022, according to data provided by the consultants. In 1Q2023, 70% of the properties transacted (5,742 units) were residential.

Saleha says: “The residential subsector is experiencing steady growth driven by Penang’s growing economy and the state being one of the top expatriate destinations. The residential subsector attracts not only local home buyers but also investors. Besides, the demand for affordable housing remained high — 73% of transacted residential properties in 2022 were below RM500,000.”

Henry Butcher’s Teoh notes that Penang’s industrial and manufacturing sectors have always been the backbone of the state’s economy, contributing 47.3% of its gross domestic product in 2021.

According to him, Penang — dubbed the Silicon Valley of the East — is home to more than 350 multinational corporations specialising in semiconductor manufacturing, electrical and electronics (E&E), and consumer electronics, which are supported by over 3,000 manufacturing-related small and medium enterprises.

“Factors contributing to the success of Penang’s industrial sector include a strong and vibrant E&E ecosystem, skilled workforce, government support, as well as well-planned infrastructure and connectivity,” says Teoh.

He adds that the industrial property subsector is leading the pack, with demand outstripping supply. “Higher selling prices and rents are observed. This segment is now clearly a sellers’ market as opposed to the other segments, which are confronted with issues of perceived oversupply, overhang and overpriced.”

As for the hospitality sector, including hotels, retail outlets and F&B establishments, they are poised to do well, given the increase in local and foreign tourist arrivals, says Teoh. “The opening of the China market will undoubtedly have a strong significant impact. Medical tourism and MICE (meetings, incentives, conferences and exhibitions) are supporting the hospitality industry as well. Heritage pre-war homes and shops are another asset class seeing remarkable growth in capital values over the years due to the inelastic supply and strong demand.”

Development hotspots

Batu Kawan, the third satellite town in Penang after Bayan Baru and Seberang Jaya, and its immediate surroundings in Seberang Perai have become a development hotspot in the state.

Batu Kawan has experienced the most development activities in recent years, says CBRE | WTW’s Peh. “The catalysts for this is the second Penang bridge (Sultan Abdul Halim Muadzam Shah Bridge) linking Batu Kawan to Bayan Lepas on Penang island, the establishment and maturing of the Batu Kawan Industrial Park, and the availability of sizeable development land for township development.”

Henry Butcher’s Teoh notes that Bandar Cassia in Batu Kawan, which is in the Seberang Perai Selatan district, is seeing the most development activities. “There are several ongoing developments in Bandar Cassia, including Vivo Executive Suite, Versa and Viluxe by Aspen Group; Beldon and Camdon by EcoWorld; Anggun Residences by PE Land; Savana by Paramount Group; ION Vivace by Grand Flo; Columbia Asia Hospital; and a petrol station.”

The well-planned infrastructure and strategic location of Bandar Cassia are the major factors contributing to the success of this satellite township, he adds.

“Developers and investors are eyeing the potential spillover effect from the vibrant industrial sector in Penang, especially the Seberang Perai Selatan district, which has created a lot of job opportunities and improved the living standard in that area. The prices of landed properties and high-rise condominiums as well as serviced apartments in the area are now on a par with those in the southern part of Penang island.”

Nawawi Tie Leung’s Saleha notes that in addition to Batu Kawan, locations like Kepala Batas, Bertam and Tasek Gelugor are also seeing active development activities. “The catalysts include nearby industrial parks, which offer employment opportunities to the locals; new industrial parks to accommodate the growth of the manufacturing sector, especially E&E; and township developments that provide all-in facilities and amenities offering a lifestyle suitable to the preferences of today’s target market.”

Meanwhile, major land reclamation works for the upcoming Seri Tanjung Pinang Phase 2 as well as the proposed Penang Silicon Island (previously known as Island A of Penang South Island, or PSI) as well as the light rail transit component of the Penang Transport Master Plan (PTMP) are expected to be the main catalyst that will change Penang’s landscape and provide new opportunities for the property market, says Peh.

Residential

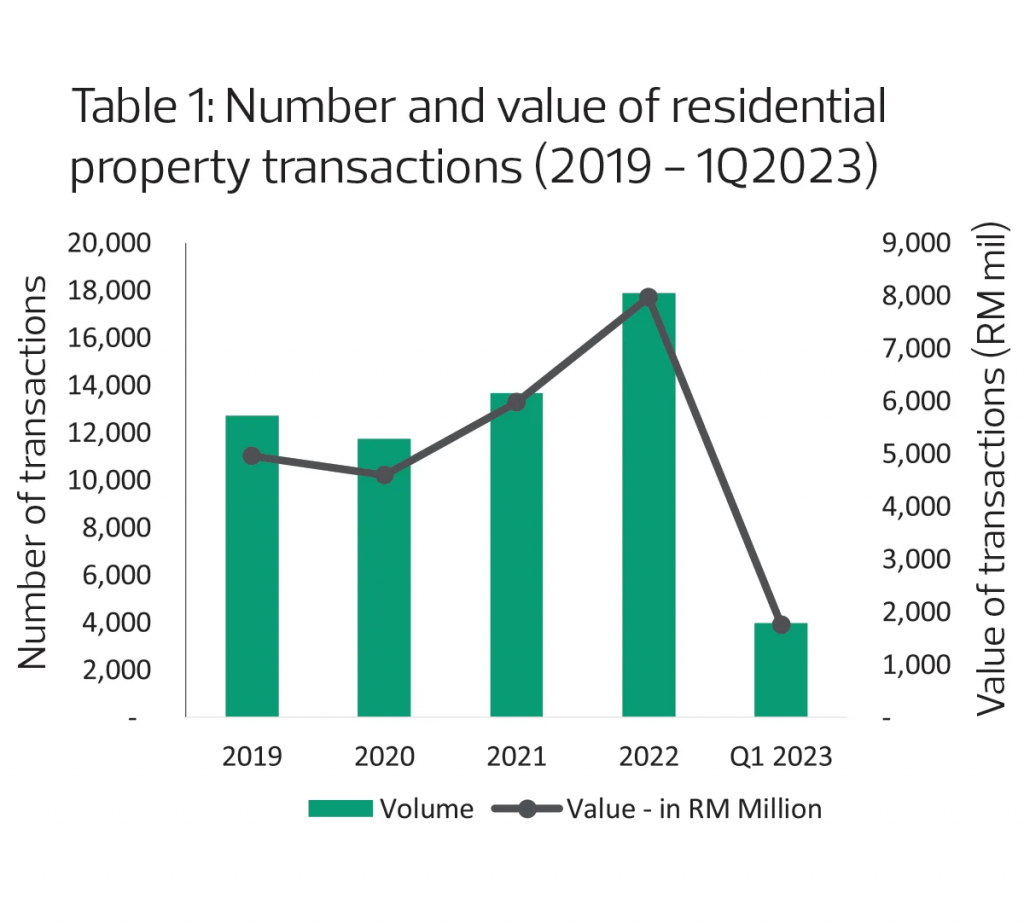

Penang’s residential property market was active in 2022. According to Nawawi Tie Leung Property Consultants Sdn Bhd executive director Saleha Yusoff, the volume and value of transactions have increased steadily over the past three years, with 11,736 transactions worth RM4.58 billion in 2020; 13,648 transactions valued at RM5.97 billion in 2021; and 17,892 transactions worth RM7.96 billion in 2022.

The total transactions on Penang island stood at 8,305 units, of which 23% were landed and 77% were high-rise. On the mainland, the total transactions came to 9,587 units, of which 73% were landed and 27% were high-rise, Saleha notes (see Table 1).

“In the short and medium term, we expect demand will continue to be strong due to better job opportunities based on the number of new investments announced in the E&E and medical sectors. The rising material and labour costs have continued to be challenges faced by the residential property market. Hence, developers are focusing on their unique selling propositions, or USPs, that are relevant to their target market to control costs while offering units that are affordable to potential buyers,” says Saleha.

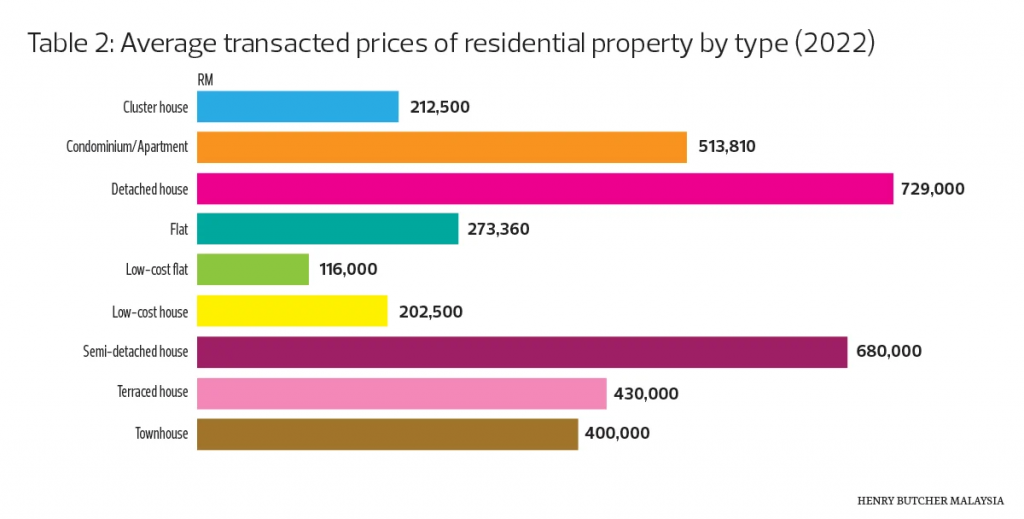

Henry Butcher Real Estate (Penang) Sdn Bhd director Teoh Poh Huat observes that the state’s residential property segment saw a sharp year-on-year increase of 31% in volume and 33% in value in 2022. “Of the total [17,892 transactions], 7,635 units or 42.67% were landed property transactions (terraced, semi-detached, detached and cluster homes) with a total transaction value of RM4.42 billion, indicating an increase of about 20.8% in volume and 23.7% in value compared to 2021,” he says.

“For condominiums and apartments, a total of 3,749 transactions worth RM2.297 billion was recorded in 2022 compared with 2,353 transactions worth RM1.367 billion in 2021, a sharp increase of about 59% in volume and 68% in value,” he adds (see Table 2).

In terms of the high-rise residential property segment, CBRE | WTW director Peh Seng Yee says a buyer’s market exists due to the significant number of overhang units. “There is a price correction in the primary as well as secondary markets, thus there is opportunity for bargain hunting.

“As for the landed residential property segment, there has been relatively limited supply of new units. Therefore, the prices of landed homes have been resilient and are holding well. They are expected to increase over time in line with the rising construction costs.”

According to Peh, condominium and apartment units made up the bulk of residential property transactions in Penang in 1Q2023, totalling 889 or 22% of the residential properties transacted. “The transacted prices of condominium and apartment units came to RM561.96 million, which is an average of about RM630,000 per unit,” he says.

“Two- and three-storey terraced houses saw the second highest residential property transactions at an aggregate of 855 units worth RM432.41 million, which is an average of about RM505,000 per unit.”

In terms of outlook, Peh expects “the recovery in market activity of the residential property sector to spill over to the short term amid challenges of the rising cost of living and higher interest rates, which are generally dampeners to sentiment of consumers that will impact residential property transactions”.

“While a buyer’s market will still be prevalent for the high-rise residential property segment, the prices of landed residential units will be resilient. Future launches are anticipated to trend towards self-sustained developments, smaller scale and fulfilling the pent-up demand for affordable units,” he adds.

According to Teoh, the notable increase in the value and volume of residential property transactions in 2021 and 2022 can be largely attributed to two key factors — the historically low interest rates and the implementation of the home ownership campaign (HOC). The HOC, which was introduced by the government to promote homeownership and reduce the number of unsold residential properties in the country, ended in December 2021.

Despite the challenges potential buyers and property developers face, Teoh expects the residential property market in Penang to remain healthy, thanks to the thriving industrial sector in the region as well as the strong performance of the medical and tourism sectors on Penang island. “These dynamic sectors in Penang are anticipated to indirectly stimulate the demand for housing,” he says.

Saleha believes that Penang’s residential property market will continue to be active with the implementation of federal and state government initiatives and policies, as well as the ongoing infrastructure developments. “The residential property market will continue to focus on the affordable and mid-range segments to meet local demand. In areas with high investment potential, fully furnished small to mid-sized units have gained appeal among local and international investors,” she says.

She adds that with an ageing population and Penang’s increasing popularity as a retirement destination, professionally managed senior living (independent living, assisted living and aged care residence) with medical/healthcare facilities will be in demand.

Retail

Penang’s retail property segment is experiencing a gradual recovery from the slowdown caused by the pandemic, says Henry Butcher’s Teoh. “Over the past five years, retail property prices in Penang have generally remained stable due to the lack of significant changes in rental rates,” he says.

“However, there are certain new and upcoming commercial developments in Penang, such as Iconic Point in Simpang Ampat and Borealis in Batu Kawan, both located in Seberang Perai Selatan, which have achieved record-breaking transaction prices and rental rates in their respective areas. These developments have introduced innovative concepts and demonstrated excellent occupancy rates.”

Further, Teoh observes that prime shopping complexes such as Gurney Plaza, Gurney Paragon, Queensbay Mall on Penang island and Sunway Carnival Mall on the mainland, have shown improvements in terms of footfall and occupancy rates. “These malls have been hosting an increasing number of commercial activities at their concourse areas during weekends and festive seasons.”

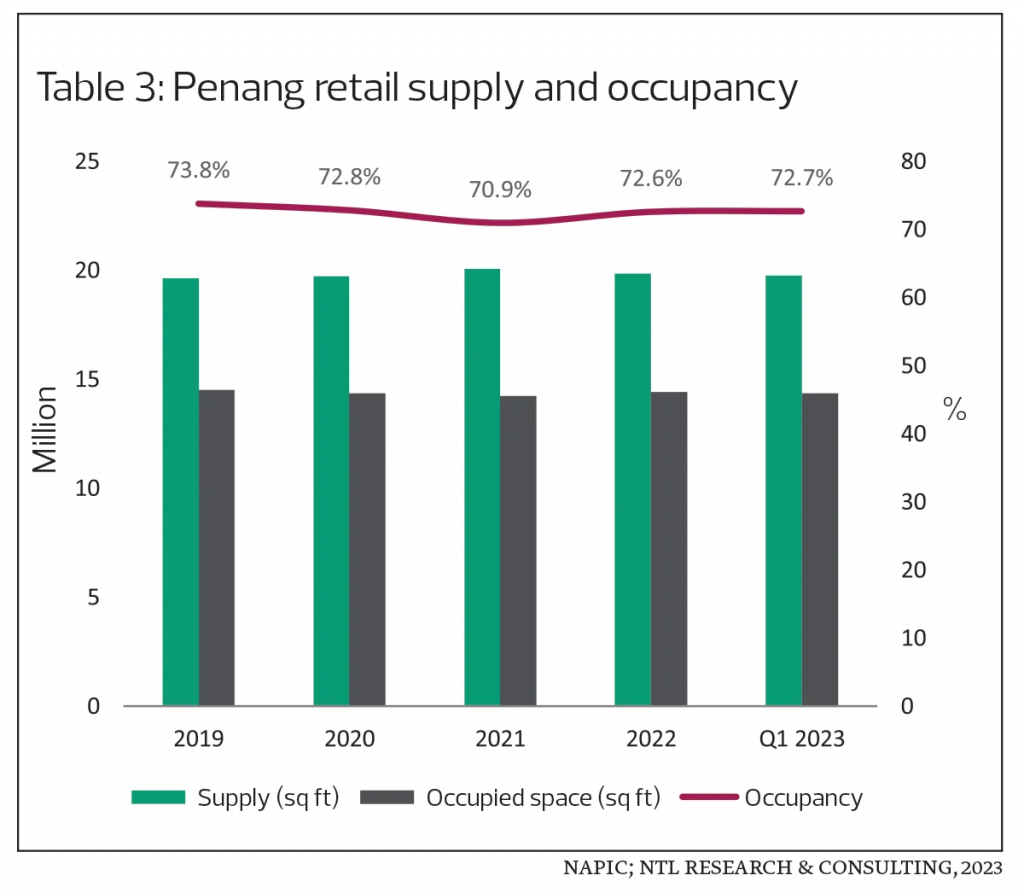

Meanwhile, Penang has a total shopping complex retail space of 1,844,184 sq m, with an average occupancy rate of about 73% as at 2022, he notes.

Nawawi Tie Leung’s Saleha has observed a surge in the number of transactions of shopoffices, from 623 units in 2021 to 1,044 units in 2022, making up 55% and 64% of the total commercial property transactions respectively. “The opening of new townships has attracted buyers to invest in shopoffices to provide daily conveniences, especially in areas with limited amenities,” she says.

In 1Q2023, there were 789 transactions, 488 — or 60% — of which comprised shop units or retail lots in mixed-use developments, she adds. “The integration of commercial and residential components, such as the Queens Waterfront development, gives buyers the confidence to invest in shop/retail units as the project offers sustainable on-site demand.”

Nonetheless, Saleha cautions that the developers of mixed-use projects must ensure the local market can support the amount of commercial space these offer, be it retail or office.

In terms of Penang’s retail property supply, she says it had grown at a compound annual growth rate (CAGR) of 0.4% between 2019 and 2022. “During the period, the occupied retail space recorded a negative CAGR of 0.2%, leading to a decline in the occupancy rate from 73.1% in 2018 to 72.6% in 2022,” she says.

There is an incoming supply of 2.68 million sq ft in net lettable area (NLA), including Sunshine Mall in Farlim (NLA: 800,000 sq ft), which will open by December 2023; GEM Megamall in Seberang Jaya (NLA: 1.2 million sq ft), which is slated to open in 2026; and The Waterfront Shoppes at The Light City in Gelugor (NLA: 680,000 sq ft), which is expected to open in early 2025.

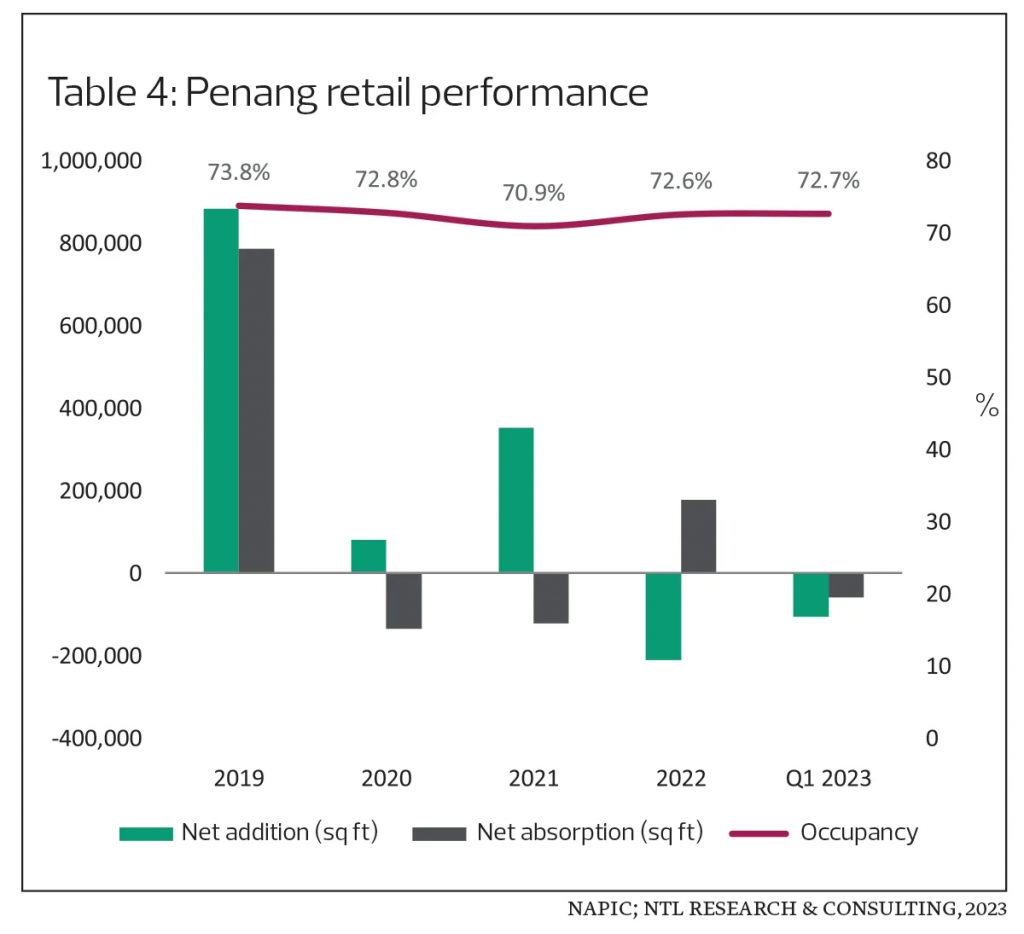

Between 2019 and 2022, the average net addition of retail supply was about 276,000 sq ft while the average net absorption rate was about 177,000 sq ft, according to Saleha. A notable opening in 2019 was IKEA Batu Kawan, which is part of a 1.6 million sq ft retail complex now known as Klippa Shopping Centre (see Table 3 and Table 4).

She notes that the high transaction value in 1Q2023 (RM2.485 billion) was likely contributed by the completion of CapitaLand Malaysia Trust’s RM990.5 million acquisition of Queensbay Mall, which involved 91.8% of the total strata floor area of retail parcels in the mall.

In terms of existing malls, their occupancy rates remained stable between 71% and 74%, though Saleha notes that a healthy rate is considered to be above 80%. “With the incoming retail supply of about 2.68 million sq ft in NLA, we expect competition to intensify,” she says.

However, the retail scene will be more exciting with new-to-market retailers, she adds. For example, GEM Megamall has announced the Sogo department store as the anchor tenant and the first in the northern region. “With the return of tourists to Penang, we expect more retail activities in the heritage area. Many pre-war shops have been converted into interesting cafés, offering more F&B diversity and options.”

According to CBRE | WTW’s Peh, the occupancy rate at shopping complexes was nearly 80% on Penang island and 63% in Seberang Perai. “Rental revision has not been positive and quite flattish,” he says.

He notes that the state’s retail property subsector went through a V-shaped recovery in terms of retail traffic following increased vaccination rates and easing of lockdown restrictions in 4Q2021. “Malaysians have been travelling and spending more domestically. The normalisation of shopping activities has been rapid, spurred by the ‘freedom euphoria’.”

In terms of outlook, he says, the retail industry will continue to see normalisation amid the challenges, including the spike in inflation, which will reduce purchasing power, escalate the cost of living and increase the operating cost of businesses. “With major new complexes entering the market, the shopping experience will be exciting but the performance gap between the newer and older retail complexes will be wider.”

Teoh is optimistic about the state’s retail industry and anticipates a favourable outlook in the mid and long term, thanks to the thriving tourism industry in Penang. “This can lead to a surge in demand for retail space in the future,” he says.

“In the mid term, the retail sector is forecast to witness a gradual recovery as the pandemic subsides and consumer confidence increases. Retailers may have to adopt new strategies and technologies to adapt to the changing market landscape and meet evolving customer needs.”

He believes that in the long term, the retail industry in Penang is likely to grow due to the area’s growing population and strong economic fundamentals. “Retailers need to keep up with changing customer preferences and expectations, such as the emphasis on sustainability and ethical practices,” he says.

Office

The office workplace still plays an important role for face-to-face interactions and team collaborations, says CBRE | WTW’s Peh. “During the pandemic, most of the service sector retained their existing office space with certain arrangements for employees to work from home. Hence, purpose-built offices (PBOs) were one of the resilient property subsectors in Penang and were relatively less affected by the pandemic.”

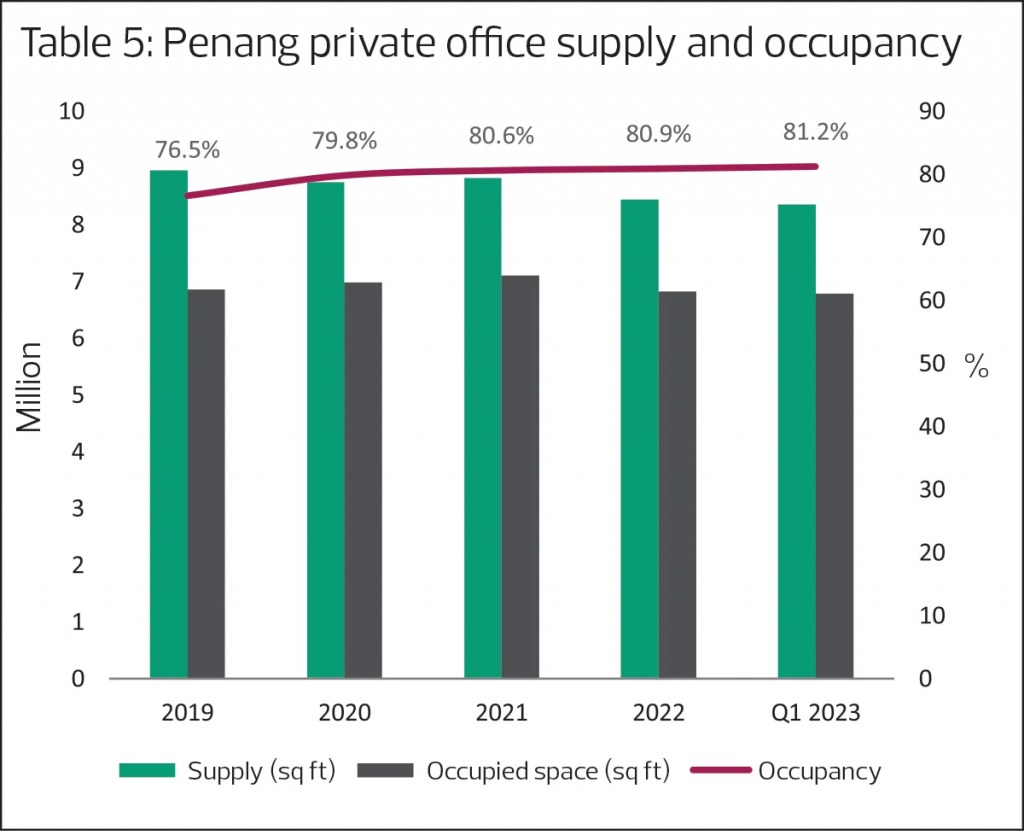

He notes that the overall occupancy rate for PBOs has been quite stable at about 87% on Penang island and 56% in Seberang Perai. The overall occupancy rate for the entire state is almost 81%.

Peh has observed a recent increase in PBO rents in Penang. “This is due to the higher quality of space offered in the market, from the relatively newer buildings as well as landlords asking for high rates to cover escalating maintenance costs due to the significant inflation lately.”

According to him, the monthly gross rent of prime PBOs located in the northeastern part of Penang island, which includes George Town and Seri Tanjung Pinang, range from RM2.40 to RM5 psf. Meanwhile, PBOs in the southeastern part of Penang island, which includes Gelugor and Bayan Baru, command higher monthly gross rents, ranging from RM3.10 to RM5.20 psf, owing to the demand from multinational corporations and local companies, as well as its proximity to the Bayan Lepas Industrial Park.

In terms of outlook, Peh expects the prevailing healthy market to continue in the short term following the expected uptick in economic activities. “Companies that have a long-term view of the market would uphold that a high-quality office space is vital to portray their corporate image as well as in valuing their employees in order to attract, retain and nurture top talent. The demand for Multimedia Super Corridor-status office space is anticipated to persist,” he says.

Henry Butcher’s Teoh highlights that the state’s total PBO space as at 2022 was 1.075 million sq m, of which 783,709 sq m —or 73% — were private buildings and 291,718 sq m — or 27% — were public buildings.

According to him, private buildings recorded an average occupancy rate of 81% while public buildings saw close to 99%. “The performance of Penang’s office property sector has been generally stable over the past five years in terms of transacted prices and rental rates,” he says.

Teoh notes that there were no PBO buildings completed in 2022. Meanwhile, the upcoming 18-storey Sunshine Tower in Air Itam town centre, which is expected to be completed this year, saw more than 60% of its office space taken up, including an eight-level tenancy by Citigroup.

In terms of average transacted prices, Teoh says those of stratified office space in prime PBO buildings such as Gurney Tower, Menara Northam, Maritime Piazza and e-Gate were between RM450 and RM750 psf, depending on the location, size/floor area, layout, condition/renovation and view of each unit.

He defines prime properties as typically located in major commercial centres with good accessibility to public transport, have quality design, are energy and environmental, social and governance (ESG) efficient and have Grade-A tenants. “The absence of any of these criteria means that an asset will generally be rated as secondary property.”

For stratified office space in secondary office buildings, the transactions on the secondary market were generally below RM350 psf, says Teoh. “These buildings are normally quite old [built in the 1980s], lack maintenance, have outdated facilities, limited parking space and larger floor areas compared with modern PBO buildings.”

As for rental rates, he highlights that stratified PBO space in prime office buildings command a monthly rent of between RM3 and RM4.50 psf, while stratified PBO space in secondary office buildings fetch RM1.80 to RM2.80 psf.

“There is a growing demand for new office buildings with better specifications and MSC status due to the increasing demand for global business services. In the short term, the Penang office market is expected to remain stable in terms of prices and rental rates. However, the mid- and long-term outlook depends on various factors, such as the economic performance, population growth, business investment and demand for office space,” says Teoh.

“If the economy continues to grow and attract businesses, the demand for office space could increase. Nevertheless, challenges could arise if there is an oversupply of office space or an economic slowdown. It is also vital to consider unpredictable events such as natural disasters or pandemics that could impact the outlook for the office segment.”

According to Nawawi Tie Leung’s Saleha, Penang’s office supply recorded a negative CAGR of 2% between 2019 and 2022. This could be due to the repurposing of vacant or old office buildings into other uses such as hotel, serviced apartment, confinement centres, nursing homes, rehabilitation centre or educational institutions, she says.

“During the period, the occupied office space declined at a negative CAGR of 0.1%. However, as more supply disappeared from the market than demand, the occupancy rate was on an [upward] trend, even though the demand was lower,” she says.

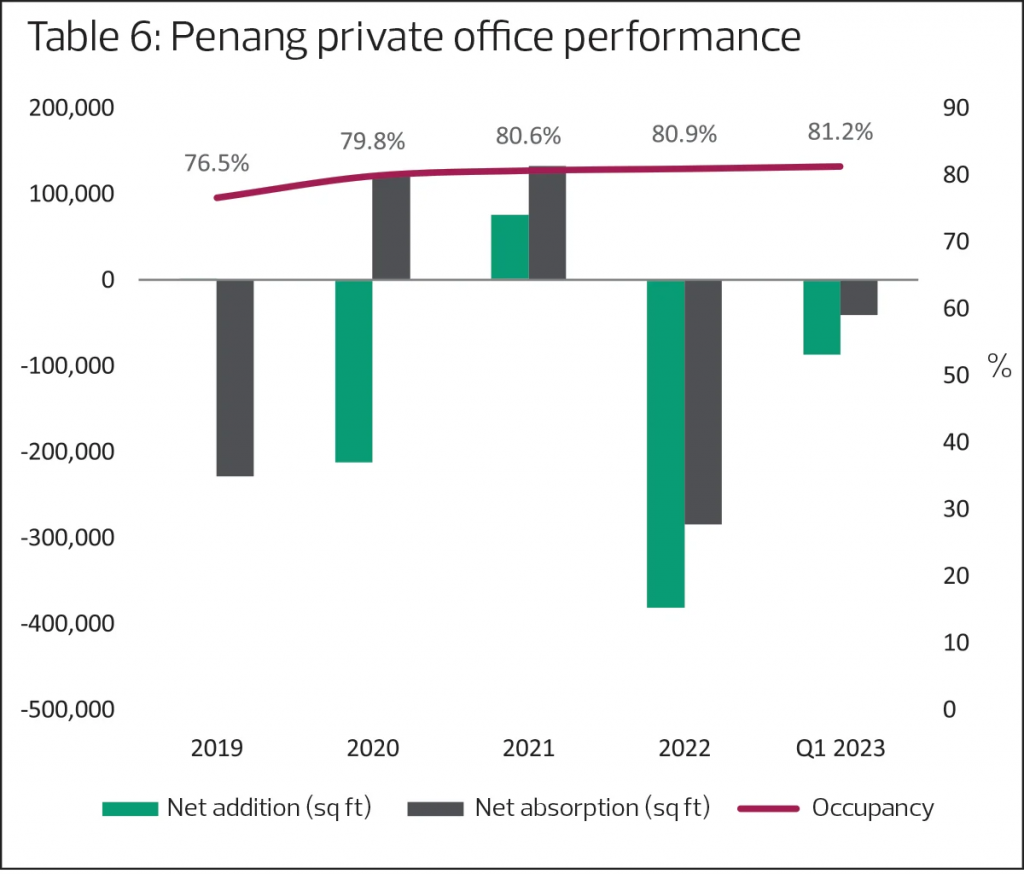

Based on National Property Information Centre data, Saleha notes an incoming supply of 800,000 sq ft of NLA in the Penang market, which includes VOS Lifestyle Suites, Sunshine Tower and GBS by the Sea. “As at 1Q2023, the average net addition was about -129,000 sq ft, while the average net absorption was about -65,000 sq ft because the supply had been decreasing on a yearly basis,” she adds (see Table 5 and Table 6).

The Penang office market was quite active, says Saleha. In addition to Citigroup taking up office space in Sunshine Tower, AMD Global Services has also been announced as an anchor tenant (occupying 70%) of GBS by the Sea.

“With the completion of GBS @ Mayang and GBS Mahsuri, and the upcoming GBS by the Sea, Penang has established itself as one of the emerging GBS centres in Southeast Asia. Should Penang continue attracting more GBS companies, these companies will create job opportunities and demand for office space. The presence of GBS players will also create a multiplier effect in other property subsectors such as residential, retail, healthcare and education,” she says.

Industrial

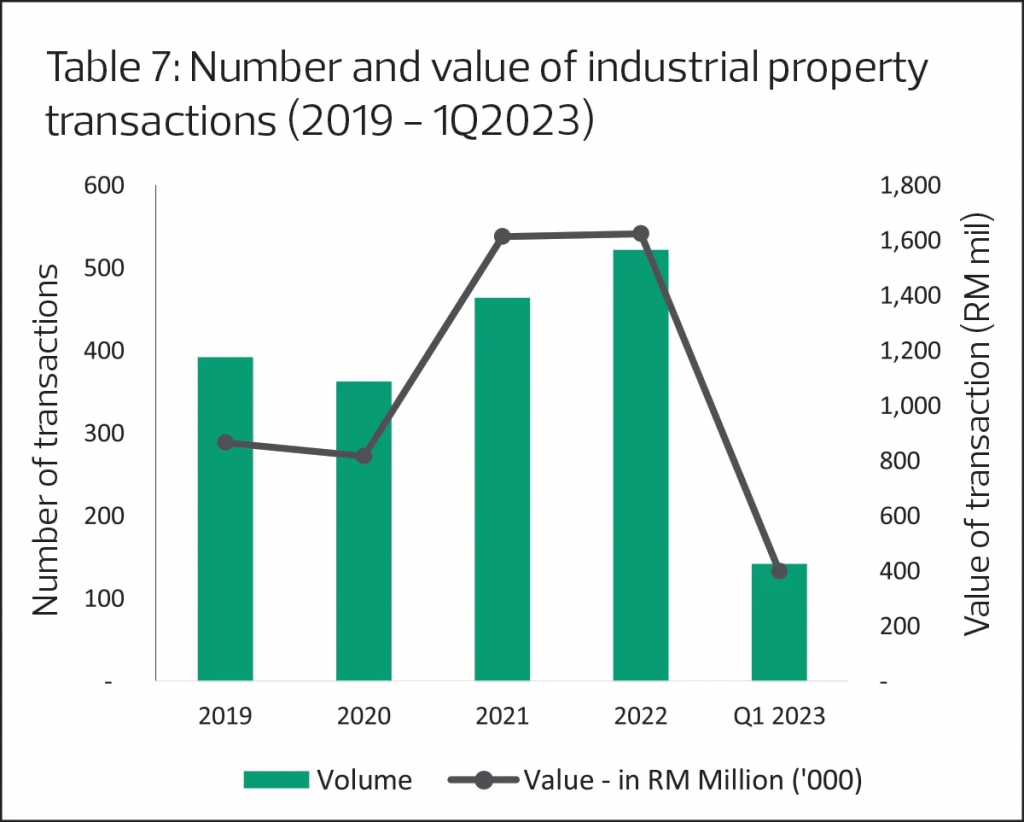

The industrial property market in Penang is showing positive signs of growth, with the highest number of transactions recorded in 2022 (522 units) since 2019, says Nawawi Tie Leung’s Saleha (see Table 7).

“Penang’s growing economy and attractive investment incentives make it an attractive destination for domestic and foreign investors, especially in the manufacturing sector. This growth has prompted developers with land bank along highways to develop integrated industrial parks targeting light and medium high-tech industries,” she says.

However, despite the availability of international standard infrastructure like transport network, utilities and telecommunications, Penang’s industrial property market faces some challenges such as the global economic uncertainty, as many of the investments in manufacturing come from multinational corporations, and rising construction costs.

Nonetheless, the demand for industrial properties remains strong in Penang, mainly from the E&E and medical device sector, says Saleha. “The continuous flow of investments, especially in the E&E and medical device sectors, has resulted in the expansion of industrial developments in Penang by various developers.”

Henry Butcher’s Teoh notes that the 522 industrial property transactions worth RM1.623 billion in 2022 indicate a 12.5% increase in volume and a 0.7% increase in value from 2021. Leading the number of transactions were terraced factories/warehouses (183), followed by semi-detached factories/warehouses (122), industrial vacant plots (104), detached factories/warehouses (68) and others (13).

“In terms of volume, the Seberang Perai Tengah district was a dominant force in terms of industrial transactions, chalking up 50% of the total transactions. This was followed by Seberang Perai Selatan (20%) and Seberang Perai Utara (15%),” he adds.

For vacant industrial land, prices have generally risen between 5% and 15% in Seberang Perai compared to 2021, says Teoh. “The transacted prices of industrial land in Seberang Perai ranged from RM40 to RM65 psf depending on the location and tenure.”

Meanwhile, he anticipates that the industrial sector will continue to perform well this year, supported by its transition to Industry 4.0 and the high rate of digitalisation. “Penang has made a name for itself as a significant regional hub for electronics production, thanks to the presence of a large E&E cluster. The pandemic accelerated raw material sales, strengthening Penang’s position in this sector. Rapid technical breakthroughs and digitalisation, which have raised the demand for industrial properties in the area, [also contributed to] the state’s expansion as a manufacturing powerhouse.”

The growth of Batu Kawan Industrial Park 2 (BKIP2) by 1,500 acres and BKIP3 by 600 acres points to a bright future for Penang’s industrial real estate industry, he adds. “The lack of huge land parcels and rising demand are the driving forces behind this expansion. Overall, despite the fact that there are several opportunities in the industrial industry, there are many worldwide challenges and market uncertainties, such as geopolitical conflicts.”

Meanwhile, Teoh says Penang will continue to benefit from geopolitics. “Performance indicators in the manufacturing sector are robust and remained resilient in the past years despite the uncertainties and supply disruptions caused by the pandemic and geopolitical tensions.”

He adds that the increase in capital values, rents and occupancy rates of production space is likely to be modest to strong due to the limited supply of industrial land and properties. “The growth prospects for the manufacturing sector will be led by the continuing digitalisation, e-commerce and technological advancements in the transport, engineering and semiconductor segments. Manufacturers, related suppliers and logistics players are anticipated to consider Penang as their regional base, given its stable fundamentals and proactive state and federal government initiatives,” he says.

“Sectors that will appeal to investors include business space, life sciences, industrial, data centres and logistics. Demand is expected to come from regional corporate offices of industrial companies and multinational corporations; backroom support offices of financial institutions; IT firms and R&D companies.”

CBRE | WTW’s Peh says, “Penang’s industrial property sector has grown from strength to strength with flourishing market activity. The encouraging new manufacturing investments have continued to underpin this sector.”

With Industry 4.0 requirements for high-technology implementation as well as last-mile delivery requirements for warehouses that are closer to the population catchments, there are opportunities for built-to-suit arrangements, he says.

“Owing to the ongoing corporate restructuring, there are also opportunities for sale and leaseback arrangements. Moreover, purpose-built workers’ dormitories are a growing opportunity as industrialists strive to comply with Act 446 of the Workers’ Minimum Standards of Housing and Amenities Act as well as align with the global goals of ESG,” says Peh.

According to him, land values at Penang Development Corp’s (PDC) industrial parks range from RM30 to RM60 psf in Seberang Perai and between RM80 and RM140 psf in Bayan Lepas. Asking prices of industrial parcels of land in BKIP have increased to RM70 psf.

Meanwhile, Peh expects further improvements in prices and rents in the short term, driven by healthy demand in the industrial sector.

“Owing to the availability of sizeable development land, Seberang Perai will continue to be the hotspot for new PDC and private industrial projects such as Penang Medical and Digital Technology Hub, BKIP2, Penang Science Park South, A-park, VDI, VS11 and Penang Technology Park. The strong investment performance will continue to underpin the state’s industrial property subsector,” he says.